Resume

The principal objective of this master thesis is to estimate the fair price of one Pandora share as of 31 December 2011 on a stand-alone basis. Valuation is conducted through strategic and financial assessment.

Investors were excited to participate in the Denmark’s largest initial public offering in sixteen years and in a less than a year were “shocked” to find a sudden change in revenue and profit trend. The reaction was extraordinary – share price lost two thirds in just one day. This master thesis tries to estimate whether market priced Pandora’s stock objectively or it was just a temporary overreaction.

Pandora became the third largest world jewelry company in a relatively short period. Company is atypical among largest jewelry players to operate without retail operations and focus on manufacturing. Pandora stands out to be a rare player to get such a wide acknowledgment by affordable jewelry consumers. Exceptional product charm is the primary value driver and the largest danger.

Strategic analysis shows that Pandora overcomes external environment and jewelry industry challenges with unique resources: successful product charm, state-of-the-art production facilities, inexpensive production team in Thailand, in-house designers from Denmark, revolving credit facility, highly valued brand; and core competences: extensive manufacturing experience, abilities to scale the craftsmanship, abilities to enter new markets, strong financial consolidation and control functions and win-win retail proposal.

Financial analysis reveals that Pandora reached the point when customers are not ready to pay for affordable jewelry more and should lower current prices to keep the volume stable. New markets and particularly emerging countries should remain being the most important contributors to growth, but there is a threat that the company will not be able to stabilize the revenues from mature markets. Pandora has superior profitability comparing with peers, but not sustainable in the long-term. Pandora’s ROIC is considerably higher than peers’, but has been gradually decreasing and approaching the industry average.

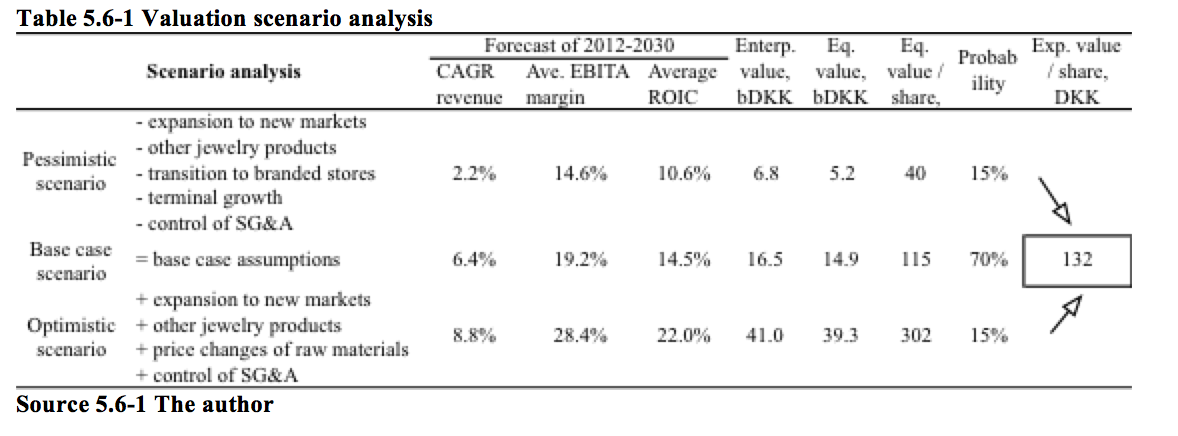

The fair price of 132 DKK per one share on 31 December 2011 is estimated with probability weighted scenario discounted cash flow value driver model. Valuation is also examined with alternative discounted cash flow models (economic profit, NOPLAT convergence, exit multiple, FCF perpetuity) and peer multiples. The outcome is tested with sensitivity analysis. Different scenarios are modeled to determine pessimistic (40 DKK) and optimistic (302 DKK) values.

The fair price is 144% higher than the market price of 54 DKK/share on 31 December 2011. The recommendation depends on the investment horizon. Investors are recommended to buy shares with long-term investment horizon and should hold shares or be aware of high volatilities in the short (from one to two years) period.

Table of Content

1. Introduction………………………………………………………………………………………………………………… 6

1.1. Problem statement…………………………………………………………………………………………………… 6

1.2. Methodology…………………………………………………………………………………………………………… 8

1.3. Thesis outline………………………………………………………………………………………………………….. 9

1.4. Benchmark……………………………………………………………………………………………………………. 10

1.5. Delimitations and data collection issues……………………………………………………………………… 10

2. Strategic analysis………………………………………………………………………………………………………. 11

2.1. Strategic position……………………………………………………………………………………………………. 11

2.1.1. External environment……………………………………………………………………………………….. 11

2.1.2. Strategic capabilities………………………………………………………………………………………….. 23

2.1.3. SWOT model…………………………………………………………………………………………………… 27

2.2. Strategic choices…………………………………………………………………………………………………….. 28

2.2.1. Business level directions…………………………………………………………………………………….. 28

2.2.2. Corporate level directions………………………………………………………………………………….. 29

2.2.3. Strategic modes………………………………………………………………………………………………… 31

3. Economic and financial analysis………………………………………………………………………………… 33

3.1. Income statement analysis……………………………………………………………………………………….. 33

3.1.1. Income statement reorganization………………………………………………………………………… 33

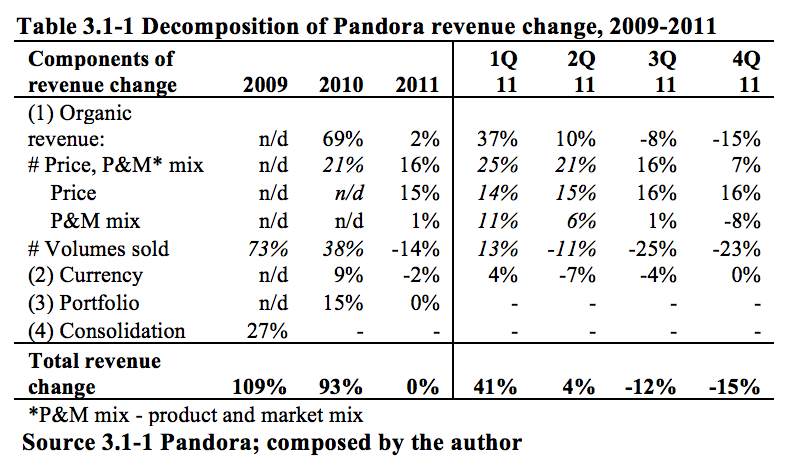

3.1.2. Revenue growth analysis……………………………………………………………………………………. 33

3.1.3. Profitability analysis…………………………………………………………………………………………. 35

3.2. Balance sheet analysis……………………………………………………………………………………………… 38

3.2.1. Balance sheet reorganization………………………………………………………………………………. 38

3.2.2. Invested capital analysis…………………………………………………………………………………….. 38

3.3. Cash flow statement analysis……………………………………………………………………………………. 41

3.3.1. Cash flow statement reorganization…………………………………………………………………….. 41

3.3.2. Decomposition of cash flows……………………………………………………………………………… 41

3.4. Combinative financial analysis………………………………………………………………………………….. 42

4. Forecast…………………………………………………………………………………………………………………….. 44

4.1. Forecast of revenues……………………………………………………………………………………………….. 44

4.2. Forecast of profitability…………………………………………………………………………………………… 49

4.3. Forecast of invested capital……………………………………………………………………………………… 52

4.4. Forecast of free cash flow………………………………………………………………………………………… 53

4.5. Forecast of the steady growth period…………………………………………………………………………. 54

5. Valuation………………………………………………………………………………………………………………….. 55

5.1. Weighted average cost of capital………………………………………………………………………………. 55

5.2. Discounted cash flow model……………………………………………………………………………………… 63

5.3. Economic profit model……………………………………………………………………………………………. 64

5.4. Cash flow model variations………………………………………………………………………………………. 65

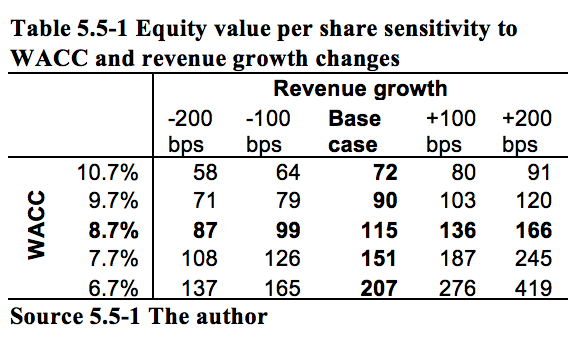

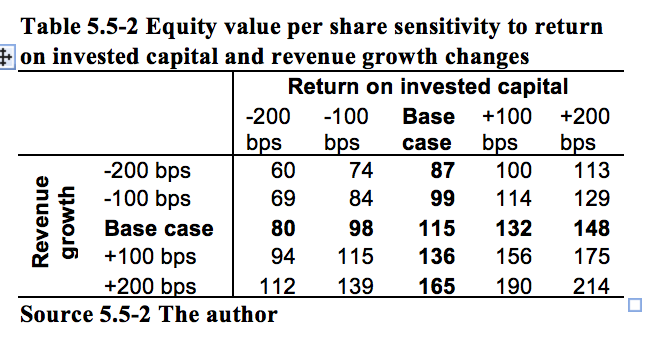

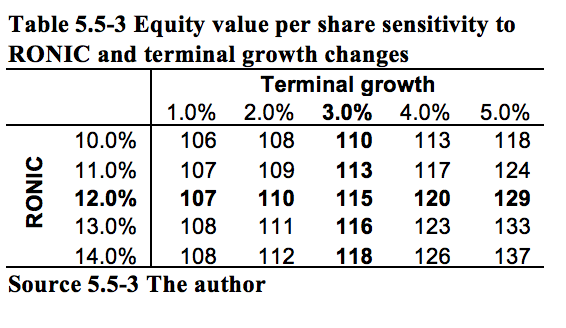

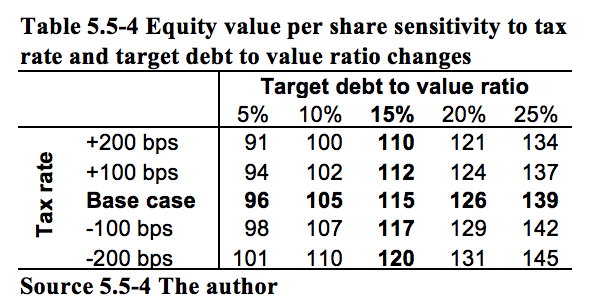

5.5. Sensitivity analysis…………………………………………………………………………………………………. 65

5.6. Scenario matrix……………………………………………………………………………………………………… 67

5.7. Multiples………………………………………………………………………………………………………………. 69

5.8. Valuation summary…………………………………………………………………………………………………. 72

6. Conclusion………………………………………………………………………………………………………………… 74

7. Perspectives………………………………………………………………………………………………………………. 80

8. List of literature………………………………………………………………………………………………………… 81

9. Appendices………………………………………………………………………………………………………………… 89

1. Introduction

In a single day, 2 August 2011 Pandora lost about two thirds of its market value in Copenhagen stock exchange trading after cutting its annual forecast and announcement chief executive officer has left. Pandora has Denmark’s largest public stock sale in sixteen years and largest daily decline in market value of 12.5 bDKK. Company has a market value loss of 40.8 bDKK from the stock peaked in January 2011 to the end of 2011 (Wieneberg, 2011; Pandora, 2011a).

Pandora price – investorship.uk

“Credibility and visibility is now completely shot,” an analyst at Jefferies International, said in a note, adding he’s reviewing his “buy” recommendation on the stock. “Investors may regret ever opening this box of disappointments.” Revenue rose 3.6% to 1.39 bDKK and operating profit fell to 440 mDKK in 2Q 2011, missing the average estimate of respectively 1.73 bDKK and 611 mDKK in a Bloomberg survey of four analysts. On top of that, July sales plummeted about 30% (Wieneberg, 2011; Pandora, 2011a).

The results, published two weeks earlier than scheduled, are “totally unacceptable” and “self-inflicted,” chairman Allan Leighton said at a conference call with analysts. Pandora was wrong to have increased prices, he added. “We have been doing that at a time when consumers have become more value conscious,” he said. “We will move back to where we really should be, which is within affordable luxury” (Wieneberg, 2011; Pandora, 2011a; b).

Pandora altered forecast of 30% growth to zero growth. Company will suspend planned price increases this and upcoming year, will start a strategic review using external consultants, and will present the conclusions to investors at the end of 2012, A.Leighton said. Chief executive officer has resigned with “immediate effect” and board member Marcello Bottoli took over the company. “The CEO of the company is in the end accountable for the performance” A.Leighton said (Wieneberg, 2011; Pandora, 2011a; b).

1.1. Problem statement

This master thesis aims to determine whether Pandora’s value declined along with the market price. Author examines all available strategic and financial factors that affect the value of Pandora with the ultimate goal to estimate the value itself. The problem statement is defined following:

Based on strategic and financial valuation, what is the estimated fair price of one share of Pandora as of 31 December 2011 on a stand-alone basis?

Strategic and financial analysis enables to project the base case, worst case and optimistic case scenarios. Suggestions are provided outside the scope of base case scenario to indicate potential valuation improvements. Core results are summarized in the conclusions and suggestions are provided in perspectives.

Valuation is done on a stand-alone basis, which implies valuation without taking into account the value of any synergies, related with merger and acquisition activities.

Assessment of the value requires comprehensive appraisal of business operations and surrounding environment. Prior issues are addressed in the following table:

| Strategic issues | Model / method | |

| Which macro (external) environment elements determine Pandora’s development? | PESTEL, SPECTACLES | |

| How does the competitive environment influence Pandora’s operations? | Porter’s 5 forces | |

| Which product characteristics are the most important for Pandora customer? | Critical success factors | |

| What distinguishes Pandora from the competitors? | Strategic capabilities | |

| Which micro (internal) elements determine the value creation process in Pandora? | Porter’s value chain | |

| How does Pandora achieve competitive advantage? | Strategy clock | |

| Which Strengths, Weaknesses, Opportunities and Threads face Pandora? | SWOT model | |

| How does Pandora position itself in terms of products and markets? | Ansoff matrix | |

| Where Pandora could be located in terms of growth and market share profile? | BBG Matrix | |

| What is the most likely strategic mode to execute strategies for Pandora? | Strategic modes | |

| Economic and financial issues | ||

| What are the operating and non-operating items within Pandora’s income statement, balance sheet and free cash flow statement? | Reorganization of financial accounts | |

| What are the main components of revenue growth rate? | Revenue decomposition | |

| Which geographical areas contribute largest revenues and highest growth? | Revenue decomposition | |

| Are Pandora’s operations superior or inferior comparing with peers? | Comparison with peers | |

| What are the key factors of Pandora’s profitability? | Profitability analysis | |

| What are the differences between Pandora and peers’ invested capital structure? | Invested capital analysis | |

| How different are Pandora’s value creating elements from peers? | Decomposition of ROIC | |

| Forecasting issues | ||

| What is the most likely development of Pandora operations in future? | Forecasting | |

| How much the base case scenario differs from management guidance? | Comparison with guidance | |

| How does strategic direction influence future operations? | Comparison with strategy | |

| How different are explicit and terminal growth projections? | Terminal growth analysis | |

| Valuation issues | ||

| What is the appropriate cash flow discount rate for Pandora? | WACC | |

| What is the cost of equity and its components? | CAPM | |

| What is the cost of debt and its components? | Synthetic rating | |

| What is the target Pandora capital structure? | Comparison with industry | |

| What is the value of Pandora’s share based on discounted cash flows? | DCF value driver, economic profit | |

| Do all discounted cash flow models provide the same estimates? | Perpetuity FCF, exit multiple, NOPLAT convergence | |

| How sensitive are discounted cash flow model assumption to input changes? | Sensitivity analysis | |

| What is the worst case, optimistic and the probability weighted valuation? | Scenario analysis | |

| What is the value of Pandora’s share based on peer multiples? | Multiple valuation | |

| Is it worth buying shares of Pandora? | Comparison with market price | |

1.2.Methodology

This master thesis is based on fundamental analysis, which comprises thorough analysis of financial statements, company’s business health, management capabilities, competitive advantages, company’s competitors and markets.

This master thesis primarily relies on literature study. Overall theoretical valuation framework is taken from valuation guide written by McKinsey & Company’s consultants Koller, Goedhart and Wessels (2010) and applied corporate finance manual written by Stern School of Business professor Damodaran (2011). Strategic analysis is based on approach of Johnson, Scholes and Whittington (2008).

This paper is based only on secondary sources that are accessible to public. The sources are sufficiently reliable, since most of the theories are applied in practice for long time and auditors or stock exchange regulations certify most of the data.

This thesis uses mostly deductive and less inductive approaches. Many existing theories are applied to arrive to the deductive conclusions and some Pandora specificities leads to inductive conclusions. Pandora financial statements are analyzed from both top-down and bottom up approaches.

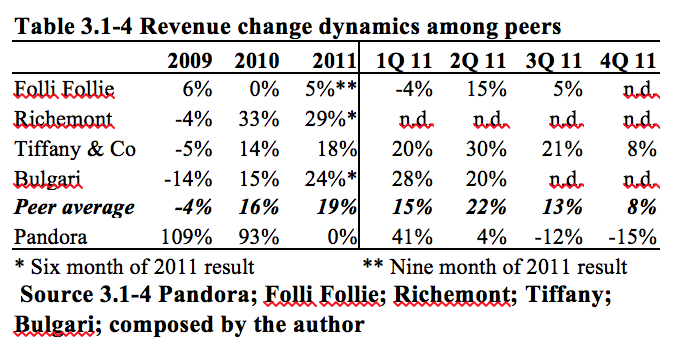

Throughout the whole paper Pandora financial performance and strategic position is compared with the peer group. Benchmarking enables to underline whether Pandora performs over or under the average. The peer group (Tiffany & Co, Richemont, Bulgari and Folli Follie) is selected based on the similarity to Pandora operations and the availability of financial data.

This master thesis is constructed so that theories and applied financial analysis are not placed apart, but are tightly integrated. Specifically, methodology is described in accordance to chapters.

Appendix 2: Presentation of Pandora is located in the appendix 2, since it is the least analytical and the most descriptive part. Company’s historic development, overview of products, ownership and stakeholder’s structure, management and corporate governance, markets and sale channels, financial and strategic highlights places the basement for further analysis.

Chapter 2: Strategic analysis unfolds the non-financial value drivers. External environment is analyzed with PESTEL and more detailed SPECTACLES models. Competitive environment is examined with Porter’s five forces models. Critical success factors reveal product characteristics that Pandora needs to pay most attention. Analysis of threshold and unique resources and competences helps to distinguish Pandora from the competitors. Porter’s value chain model helps to identify the clusters where managers should focus in order to develop more profitable business model. Strategic position is summed with the SWOT model. Strategy clock model helps to review the bases on which company might achieve competitive advantage and Ansoff matrix provides a simplified view of four alternative directions for strategic development. BCG matrix enables evaluation of the balance between the different businesses. Finally, Pandora is examined with strategic modes.

Chapter 3: Economic and financial analysis focuses on Pandora financial statements and comparison with the peers. Financial statements are normalized for comparability with peers, valuation of operating and non-operating items separately and exclusion non-recurring items. Economical and financial analysis is done with horizontal and vertical perspectives and connection with strategic conclusions. ROIC decomposition is used to depict elements of superior and inferior performance comparing with peers.

Chapter 4: Forecasting generates future revenue, income, invested capital and ultimately free cash flow projections based on strategic and financial inputs.

Chapter 5: Valuation is the core part of the thesis. WACC approach is employed to determine the discount rate and CAPM is used to detect the elements of cost of equity. The main emphasis lies on discounted cash flow value driver model, but company is examined also with DCF variations: economic profit, perpetuity free cash flow, exit multiple and NOPLAT convergence. Sensitivity analysis is designed to investigate how the changes in inputs affect the valuation and scenario analysis provides probability-weighted valuation. Valuation based on multiples estimates value comparing with peer multiple average.

1.3.Thesis outline

This master thesis is divided into eight parts. Introduction part defines the setting and presentation part portrays the object. Structurally ultimate goal to estimate the fair price is attained through strategic analysis, economic and financial analysis, forecasting and valuation. Conclusions and perspectives are drawn based on the outcomes in the final valuation part, as well as intermediary parts. Even though the main process follows the sequential order, valuation is highly iterative and interrelated process, as shown in the thesis outline figure.

Pandora – financial and strategic evaluation – master thesis – investorship.uk

1.4. Benchmark

Pandora financial accounts and ratios are compared with peers, since relative and not absolute performance displays the positioning and value in the market. In order to have a proper comparison, peer financial statements are reorganized and analyzed with similar thoroughness as it is done with Pandora accounts.

Peers are selected from the list of main Pandora competitors (Pandora, 2010a). Largest charm providers, namely Carlo Biagi, Jewelry, Bacio Italia, Chamilia and Trollbeads are not analyzed, since none of them are listed in the stock exchanges and none of them provide detailed financial statements. Peer group is assembled from the world’s largest fine jewelry players that are listed and provide financial accounts.

Comparison with the largest fine jewelry companies Tiffany & Co (later shortened Tiffany) and Richemont (mother company of second largest Cartier and fourteenth largest Van Cleef & Arpels) is in line with Pandora aims to become the world’s top jewelry firm. Seventh largest Bulgari is interesting from the perspective of what valuation could be under acquisition. Ninth largest Folli Follie is interesting as the most affordable jewelry category player. Extensive description of the peers could be found in the appendix 1.2.

1.5. Delimitations and data collection issues

Master thesis has a time and size restrictions, thus only limited amount of issues are considered. Some of the primary scope and data delimitation issues are enlisted following:

· Valuation is based on fundamental analysis and not on technical or quantitative analysis;

· Valuation is based on stand-alone basis and not on potential synergies, related with merger and acquisition activities;

· Valuation is made as a whole, on consolidated bases, not splitting up the business into parts;

· Valuation is limited with the methods described in the methodology;

· Valuation includes only secondary data, therefore, this thesis replicates the process that could be done by any investor;

· Data is collected and analyzed up to the publication of the annual report of 2011;

· Pandora’s shares are traded for the relatively short time period (from 5 October 2010) and are very volatile.

1. Strategic analysis

To evaluate Pandora’s strategic management it is necessary to understand company’s strategic position and strategic choices. Prevailing strategic position is influenced by external environment and Pandora’s strategic capability (resources and competences). Strategic choices are made in terms of direction (on a business and corporate level) and modes (Johnson, Scholes and Whittington, 2008).

1.1. Strategic position

1.1.1. External environment

Environment is divided into three layers, with increasing relevance and specifics to the company: macro-environment, industry and competitors. PESTEL framework (Oxford university, n.d.) is used to identify how the first layer, macro-environment, might influence Pandora operations.

1.1.1.1. The PESTEL framework

Among political risk factors, Thailand stands in the first place. Thailand’s political scene, fully described in appendix 3.1, has been disrupted by eighteen military coups since the end of absolute monarchy in 1932 and the situation was not much better for the last five years. Pandora was once affected in 2008, when political unrest resulted in the shutdown of the airports in Bangkok, which adversely affected company’s ability to ship products out of the country for a few days (Pandora, 2010a; EIU, 2011a).

The incoming Thailand’s administration is expected to pursue populist economic policies: introduce and by 2020 triple uniform minimum daily wage, but appease businesses by lowering the corporate income tax rate. Pandora locates all manufacturing facilities in the country and thus is directly dependent on its political and partly economical status.

Pandora is dependent on beneficial Thailand’s tax treatments, fully described in appendix 3.2. Thailand’s board of investment approved the latest Pandora’s application for tax benefits for the next five-years, but there can be no assurance that such further tax benefits will be granted on equally favorable terms, or at all. Pandora had an effective tax rate of 18% with tax benefits and 30% without benefits in 1H 2010 (Pandora, 2010a; 2011f).

Pandora might be affected by nationalistic policies that support local producers and restrict import. Nationalism tends to grow particularly in the economic recession time. Even though Pandora’s main markets are liberal and mature, company might face the difficulties in the new markets and even mature markets could surprise, as described in appendix 3.3.

Given the significant number of Pandora entities in different jurisdictions throughout the world, company’s operations could be materially adversely affected by various governmental authorities questioning intra-group transfer pricing policies and asserting alternative claims over the taxation of profits or changing local tax rules and interpretation of tax rules. Even though Pandora follows generally accepted transfer pricing practices in accordance with OECD guidelines and consults with external experts, there is likelihood that tax authorities around the world will have different interpretations (Pandora, 2010a).

No political vulnerabilities are envisaged in raw material producing countries Mexico, Peru, South Africa, US and Australia, as described in the appendix 3.4. It is a very significant factor, since raw materials constitute 92% of costs of goods sold.

From economical environment perspective, in United States, the largest Pandora market, the Congress reached a last-minute agreement to rise the federal government’s borrowing limit, averting the threat of a technical default and reducing scope for short-term fiscal stimulus while failing to address long-term imbalances. Rating agency S&P responded by stripping the US of its AAA rating to AA+, likely pushing up interest rates over time and disrupting the operation of the repo market. According to S&P, the fiscal consolidation plan falls short of what would be necessary to stabilize the government’s medium-term debt dynamics (Standards & Poor’s, 2011).

In United Kingdom almost four years after the global financial crisis hit, economic policy remains in uncharted waters, with enormous levels of financial sector support, record low interest rates and a huge fiscal deficit of 9-10% of GDP. The uncertainty persists: a deteriorating outlook at home and abroad implies that policymakers will come under increasing pressure to provide further stimulus. As skepticism grows over the effectiveness of current policies, it is likely that more radical measures will have to be considered (EIU, 2011b; d).

If not the floods, Australia would be one of the healthiest economies due to heavy concentration on resource sector, which is now soaring (EIU, 2011c).

Germany’s toughest challenge and largest risk to stability in the nearest future is the euro area debt crisis. The euro zone crisis worsened as investors lost appetite for Greece, Italian and Spanish bonds, pushing yields to above 6%. ECB reluctantly restarted its program of bond purchases, which reduced yields but is not sustainable in the long-term (EIU, 2011e).

Pandora – financial and strategic evaluation – master thesis – investorship.uk

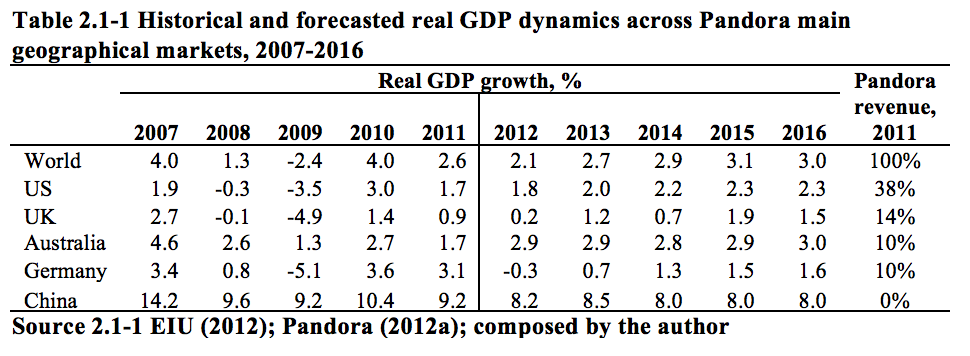

Due to concerns of a double-dip scenario, continued weakness in most economic indicators and sharp declines in the equity market, the recovery of the world economy might be slower. In the latest 2012 review The Economist Intelligence Unit (EIU) cut significantly the growth forecast for developed countries and smaller revisions were made for emerging markets, as described in the appendix 3.5.

Pandora – financial and strategic evaluation – master thesis – investorship.uk

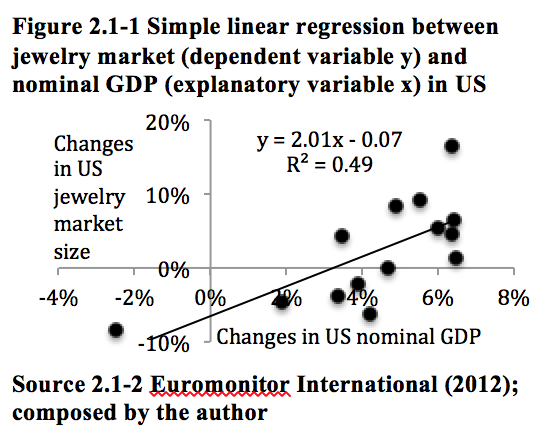

The extent to which economic development influences Pandora performance and more broadly all jewelry market is proven statistically. A data set of fifteen years changes in gross domestic product over changes in jewelry market (from 1997 to 2011) shows that 49% of movements in US jewelry market size is explained by changes in nominal GDP changes. For other Pandora markets (see appendix 3.6 for graphic views), namely UK, Germany and China the coefficients of determination are even higher, respectively 0.74, 0.88 and 0.79.

The regression functions (with the same data set) reveal that a change in the US nominal domestic product by 1% was accompanied with a 2% shift in US jewelry market. However, the jewelry market sensitivity to nominal GDP changes is lower in other Pandora markets – UK regression slope equals 1.15, Australia 0.83 and Germany 1.01. In China 1% change in nominal GDP is accompanied with 1.75% jewelry market change. The majority of regression functions supports the general understanding that jewelry industry belongs to cyclical industries with volatility being higher than the general market[1].

Pandora – financial and strategic evaluation – master thesis – investorship.uk

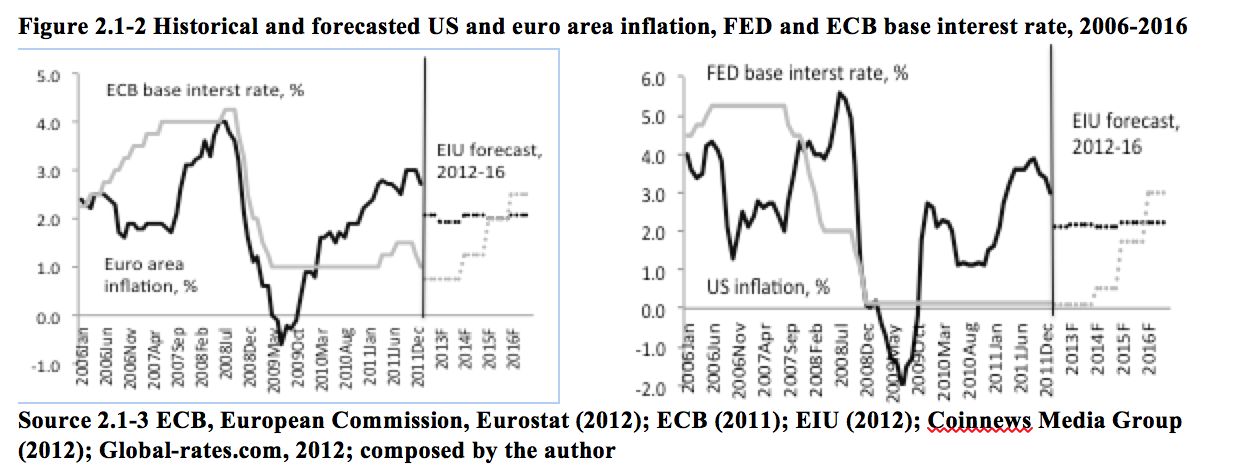

Global currency markets have become more volatile as the outlook for economic growth has dimmed and the crisis in the euro zone has intensified. The global slowdown has created a rising demand for safe-heaven currencies, in particular the Swiss franc. Pandora relevant currencies Australian dollar and Thailand baht are expected to strengthen against dollar, while British pound is forecasted to be weaker. Recently US dollar began to climb against euro as ECB raised base interest rate to fight against rising inflation.

According to new ECB president, inflation[2] is expected to remain above 2% threshold in 2012 and come down below threshold in 2013. According to EIU (2012), US inflation rate is projected to volatile at 2% threshold. Inflation assessment is done in the appendix 3.7.

Pandora – financial and strategic evaluation – master thesis – investorship.uk

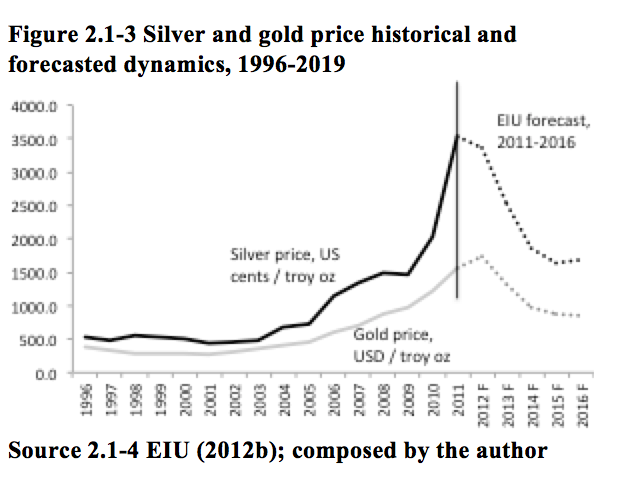

Fluctuation in prices of the raw materials is another serious concern. Pandora uses diamonds, precious and semiprecious stones, pearls, Murano glass, wood, leather, various alloys, but the main cost elements are silver and gold. Investor buying has intensified amid turmoil in the global capital markets, fuelled by anxiety over European and US sovereign debt issues, ongoing political crises in the Middle East and North Africa (MENA) region and the ultra-low global interest rate environment. In the nearest future physical and speculative demand should remain strong, while by 2013 tighter global monetary conditions and anticipation of a return to positive real interest rates should encourage some profit taking and a switch out of gold and silver, leading to a fall in prices (The London Bullion Market Association, 2012; EIU, 2012).

From employment perspective Thailand plays the most significant role, since Pandora hires in this country 69.4% of its workforce and saves a lot on wages comparing to companies employing labor in developed countries. Thailand unemployment rate in 2011 and 2010 was particularly low – only 1%. Even though the unemployment rate is expected to increase in the nearest future, it will not go above 2% for five years ahead, according to EIU (2012a). It means that Pandora will have to pay salaries at the rate of Thailand economic development.

The primary social environment driver is the customer. Pandora identifies its target end-customer as 25-50 years old woman. Company aims to fit into the affordable jewelry category, but also offers exclusive collections. Broad range of offerings enables company to reach all women within the defined age.

It is arguable whether Pandora should not go beyond the defined age and, perhaps, it is meaningful to differentiate its assortment among different age groups. The figure 3.1-5 illustrates that Pandora target age group in UK earns 56.7% of total income. It is understandable why Pandora does not target the nearest age band of 20-24 years, since it earns significantly lower portion of income (4.7% of total). However, older nearest group 50-54 earns 11.1% and 55-59 years old collects 8.6% of total income. Plus, the mean income of the last two categories is quite similar to Pandora target age group mean income figures.

Pandora – financial and strategic evaluation – master thesis – investorship.uk

Jewelry product is highly driven by fashion trends and social values. In order to forecast Pandora’s performance, it is necessary to grasp underlying trends and dynamics. To begin with, women recently started to shift from gold jewelry to silver jewelry, since silver jewelry tends to be more fashionable and affordable, according to a research by Mintel (2011 cited in CBI, 2011c). What is more important, the economic recession and high jewelry prices in Europe has affected overall consumption of precious metal jewelry to decrease and costume or design jewelry to increase (CBI, 2011d).

The same Mintel survey reveals that precious metal remains an important gift item, with 2/5 adults enjoying receiving precious metal jewelry as a birthday or Christmas present. As a result, two thirds of Pandora jewelry sales commence in the second half of the year (CBI, 2011a; Pandora, 2012a).

British women, who are often trendsetters, move away from “statement” pieces towards more refined and well-designed pieces expressing an “emotional” value and that can be worn longer. Consequently, engraved and other personalized jewelry are the popular items (CBI, 2011b). Similar trends are observed in Germany (CBI, 2011c).

Another trend is to mix and combine materials, such wooden beads, terracotta beads, shells, bones, enamel, Venetian glass, crystals, leather, rubber, ribbon, silk, coconut and copper (CBI, 2011a). As a result, costume or design jewelry is gradually taking the place of traditional precious metal jewelry. (CBI, 2011a)

Ethical jewelry and the issue of fair trade have become more important for consumers. Jewelry has widened its presence in fair trade retail outlets and ethnic groups constitute larger part of the overall population. Detailed analysis is presented in the appendix 3.8 (CBI, 2008; 2011a).

There is a growing number of working women and women in higher professional roles, which means higher levels of disposable income. For instance, in Germany working woman category expanded from 59.8% in 2005 to 65.5% in 2009. An increase took place in the older age group (55 to 64 years), while the ratio of the younger age group (15 to 24 years) decreased. As more women join the German workforce, there is a growing market for jewelry as an important fashion accessory being worn daily. In whole EU27 area, between 2005 and 2010, the ratio of working women rose from 56.3% to 58.2% (CBI, 2011c).

As the importance of social media rises, women are more influenced by on line fashion blogs, music, fashion TV or social networks. Women are also attracted by jewelry collections from celebrities as trends setters (CBI, 2011a).

Technological developments have influenced jewelry design in a variety of ways: (1) jewelers could no longer imagine industry without laser-cutting and computerized technologies, described in appendix 3.9 (JKC Magazine, 1999), (2) technology could upgrade the material, described in appendix 3.10, (3) offer more possibilities in design variations and (4) technological fusions could create a perception of innovative style.

Through technology jewelers have the ability to create and engrave variety of lifestyles and thus personalize the jewelry. Technologies provide freedom to experiment for the customer and ability to make business more efficient and profitable for companies.

The environmental issues are numerous (detailed analysis in the appendix 3.11) and become more important: mine waste, use of dangerous cyanide in gold mining, danger for the fauna. One of the peers Tiffany not only signed the pledge, but also campaigned against the mines. Activists urge jewelers to question suppliers about their gold sources and to use recycled gold (Bates, 2010).

Consumer consciousness of environmental issues grows together with acceleration by media. The green movement interweaves environmental goals with a sense of personal and social responsibility. Sustainable practices use resources without depleting them or permanently damaging the environment that yields them. For jewelers, sustainable business practices begin with analyzing their supply chain. Decent green benchmark practices include capturing and reclaiming all precious metals, encouraging customer to recycle their precious metals, controlling water usage, reducing toxic and chemical usage, reducing and recycling packaging and educating each other (Dhein, 2008).

There are numerous legal issues affecting jewelers, of which several take special attention: (1) jewelers should get warranties from their diamond jewelry suppliers, (2) dealers in precious metals and gems must establish programs to prevent their businesses from being exploited for criminal purposes, (3) jewelers must be aware of new customers, suspicious transactions, offers to pay in large amounts of money, inability to provide identification and usual payment methods, further explained in appendix 3.12 (JKC Magazine, 2004).

Importance of disclosure and description rises: (1) companies must provide detailed description of materials used, for instance, whether gemstones are synthetic, (2) sale receipts are treated as contracts, with necessity to specify what is sold and include the customer’s name, address, date of sale, customer’s signature, which acknowledges their awareness of the store’s policies, return and refund policies (JKC Magazine, 2004).

One of the largest industry concerns is copyright protection. Failure to protect adequately intellectual property enables competitors to copy the concept. In addition, many designs cannot be easily protected by copyright, because they are insignificantly different from simple standard shapes (JKC Magazine, 2004).

In addition to PESTEL’s six macro environment factors, SPECTACLES model adds four important dimensions: cultural, aesthetic, customer and sectorial.

Different cultures have different tastes for jewelry. A cultural subgroup could be differentiated by status, ethnic background, residence, religion, and position in time. Cultures tend to mix and combine different elements together with globalization, described in appendix 3.13.

In developing countries there is a growing trend of individualization and spiritual jewelry. Consumers tend to search for a deeper meaning to life, which can be eastern religions, astrology, tribalism or foreign cultures with each having its symbolic jewelry (CBI, 2011e).

While some fashion experts say aesthetically minimalism is a key fashion trend at the moment, others would say it is a never changing classic (more in appendix 3.14). Aesthetics is particularly important within stores. Store aesthetics enables to differentiate customers and influence purchasing behavior (Silwa, 2011).

Knowing how to serve different types of jewelry customers is critical. According to Tim Malone (2011), there are six distinctive jewelry shopper types to be aware: task, value and price oriented, discerning, abundance and experiential. Analysis of each type is depicted in appendix 3.15.

Since jewelry sector belongs to consumer cyclical industries, the forecasted economic “double dip” could affect jewelry companies more than market average. Another sector specific is the concentration of a substantial portion of industry’s sales in relatively brief selling periods during the year, meaning that performance is susceptible to significant periodic fluctuations.

Recently, jewelry is increasingly linking up with other sectors. This is an opportunity for the development of silver jewelry that is integrated into handbags, belts, footwear, beauty cases, eyewear, clothing, watches and electronics. There are also opportunities for accessories’ such as jewelry boxes or ring holders.

Timing and speed are very important characteristics in jewelry market. New fashion collections for seasons are usually launched at trade shows a year ago. This implies that new jewelry are developed and produced well over a year ahead of when they are on sale. Production processes need to be flexible in order to be able to respond quickly to changes in product design (CBI, 2008).

To sum-up, jewelry industry is a very fragmented and dependent on external environment. Economic factors play the most significant role, but from strategic perspective, two other factors are of key importance – social/cultural and technological issues. By foreseeing or failing to understand the coming trends in customer behavior and offer the right product to fill the need, jewelers either thrive or strive to survive.

Pandora – financial and strategic evaluation – master thesis – investorship.uk

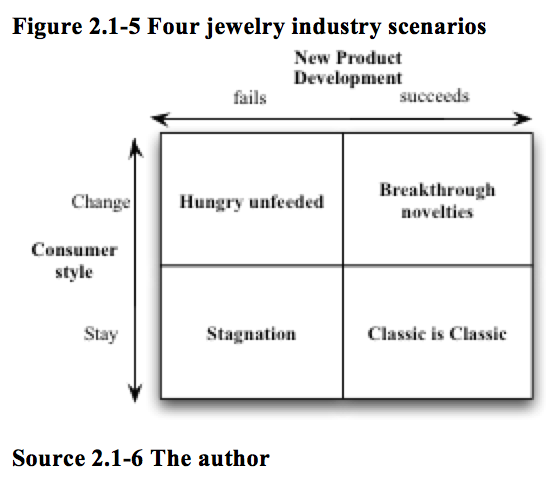

Consequently, four scenarios could possibly shape the jewelry industry: (1) under “hungry unfeeded” scenario jewelry companies are under pressure to invest more in new product development, jewelry market are volatile, fragile and with high turnover of players; (2) under “stagnation” industry gradually looses sales volume to other similar industries; (3) “classic is classic” scenario marks the resistance within discoveries, when innovators do not get return on their investment and looses incentive to invest further; (4) finally, “breakthrough novelties” offers both change of consumer style and advance in new product development, leading to growth of multinational companies.

1.1.1.2. Porter’s five forces framework

Pandora sells affordable jewelry, made of precious metals and often combined with precious and semi-precious stones and thus could be assigned to global fine jewelry market, which was estimated to be 145 bUSD in 2009. Measured on retail revenues, Pandora had a share of 1.2%[3]. Global fine jewelry market has been growing +2.9% annually from 1999 to 2009 and +4.2% excluding recent economic downturn in 2008 and 2009 (Pandora, 2010a).

The fine jewelry market can be split into three price segments: affordable (less than 1500 USD per piece), luxury (1.5 – 10 tUSD per piece) and high-end (more than 10 tUSD per piece). The affordable segment accounted for 57%, or 83 bUSD, of total fine jewelry market in 2009. Second largest segment was luxury with 29% share and the last – high-end jewelry with 15% share (Pandora, 2010a).

Affordable segment was growing at a higher pace comparing with other segments. Before economic crisis, from 2005 to 2007 annual growth of affordable jewelry was +4%, comparing with +3% growth in total fine jewelry market. At the crisis period from 2007 to 2009 annual growth rate of affordable jewelry dropped to +1%, while whole market CAGR was -2%. Affordable segment benefited from consumers trading down the luxury and high-end jewelry segments. The luxury and high-end jewelry segments were particularly affected by the economic downturn in 2009, as consumers delayed or refrained from purchases of high priced items and retailers applied heavy mark-downs to clear their inventory (Pandora, 2010a).

While the fine jewelry market has been undergoing a long-term trend toward branding across all price segments and regions, the market is still predominantly unbranded. In 2009, branded fine jewelry accounted for approximately 19.3%, or 28 bUSD, of the fine jewelry market, compared with 60%, 50% and 38% for the respective worldwide markets for watches, leather goods and eyewear. Within affordable category, branded sales constituted 24% of sales. In 2009, the top 15 global brands by retail revenue accounted for approximately 40% or 11 bUSD of the branded fine jewelry market. The remaining 60% of this market was fragmented across approximately 1000 brands (Pandora, 2010a).

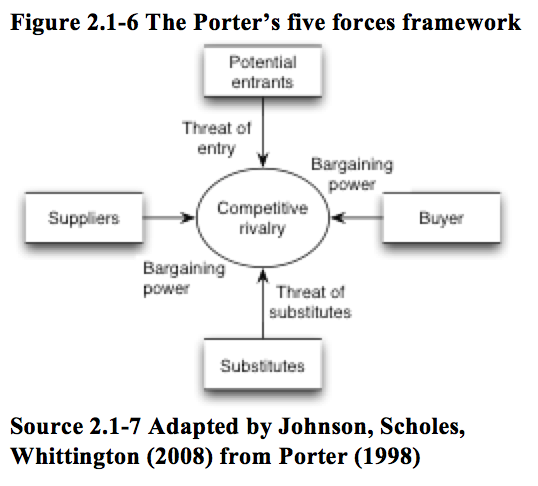

Porter’s five forces framework is useful in understanding the attractiveness and potential threats of the industry (Porter, 1998). The forces are dynamic: companies (1) destroy the barriers and enter the market, (2) build the blockades and creates threat of entry, (3) overcome barrier to enter new industry and (4) are eliminated by other competitors. Pandora is at the stage to build barriers in existing markets and break the obstacles in new markets. Jewelry industry is characterized as extremely competitive and low barricaded.

Pandora – financial and strategic evaluation – master thesis – investorship.uk

In terms of scale and experience, low investment requirements to set up jewelry company makes it relatively easy to enter the market. Economies of scale are basically inexistent, because product is not standardized and buying habits are very varying.

In terms of access to supply and distribution channels, there are numerous raw material suppliers “at the bottom” to get the materials and there are numerous multi-brand jewelry retail stores “at the top” to distribute the production. Competition is extensive at both levels.

Industry is also absent of expected retaliation feature, as existing firms do not fight with the price war after every single new player enters the market. It is also not the industry to be afraid of legal restrains.

The only significant barrier to enter is differentiation. Incumbents differentiate by selling jewelry with higher perceived value. Customer loyalty is created and maintained through combination of quality and branding.

Managers tend to focus only on competitors in their own industry and overlook the threat of substitutes, such as watches, cloth elements, handbags, accessories, perfume, cosmetics or even tattoos. There are two important elements to consider: extra-industry effects and price/performance ratio (Johnson, Scholes, Whittington, 2008). The first element is the core of substitution effect: the more substitutes become available outside the industry, the more demand of buyers is elastic and consequently industry is less attractive. Close substitution constrains the ability to raise the prices, which is one of the key important sources for profitability. Overall jewelry demand elasticity is high, but varies across different segments.

Substitutes are not only those items with similar prices, but also those that have similar or better price to performance ratio. For instance, watches are usually more expensive than jewelry, but offer important functionality – time and date output. Watches balance between style and functionality and therefore could be also assigned to jewelry category. It is therefore not surprising that Pandora is also trying to enter the market of watches. Moreover, watchmakers recently started to include various other beneficial functionalities, such as health measurement, weather forecast and calendar. As a result, substitutes should be seen from dynamic perspective, with potential to become substitutes in the future.

Clothes are usually cheaper in price and could offer less feeling of luxury as jewelry, but they also have important functionality. Clothes could also be very stylish, equally giving opportunity to show style and taste. Clothes certainly could include precious materials, which would move them closer to jewelry category.

Handbags, accessories, perfume, cosmetics or tattoos must all be also monitored through price and functionality ratio. Consumers have limited resources to spend and they could at any time shift resources from jewelry. Question of functionality becomes especially important at economic crisis time. Since jewelry has very little functionality, changing consumer habits towards functionality directly leads to losses for jewelry industry.

In addition, if to take fine jewelry separately from costume jewelry, the latter would be the most significant threat, as it is rapidly getting popular. Design jewelry is cheaper and offers wider possibilities to express creativity.

Since Pandora is a wholesale company, bargaining power of buyers is executed through retail shops, grouped into mono-brand and multi-brand resellers. Naturally the mono-brand retailers have less bargaining power, because they are reselling only Pandora product and could not easily switch to other products. The multi-brand shops have more bargaining power, but it is also very limited, since they are typically small shops or at most small retail chains. Buyers exercise their power only due to low switching cost to competitive products. Multi-brand shops offer variety of jewelry brands and if one is not successful (among ultimate customers), the order from supplier stops. The more powerful is the buyer, the lower revenues and profitability could be achieved. From Pandora perspective, mono-brand shops generate significantly higher revenues comparing to multi-brand shops.

Pandora is a vertically integrated company, thus power of suppliers is executed only from external suppliers, providing raw materials, equipment, labor force and financial capital. Most of raw materials used in production are precious or semi-precious commodities, which are traded worldwide in huge quantities. Even though two suppliers source 90% of silver supply and five suppliers provide 80% of gemstones, their power to bargain on prices is limited. On the other hand, the same is true for Pandora – it is not possible to get prices lower than quoted. From raw material production perspective, 20 silver companies produce 50% of world silver and 10 gold producers account for 78% of world gold production (The Silver Institute, 2011). As both resources are limited, prices fluctuate depending on demand, rather than production.

In terms of equipment and financial capital, Pandora has high bargaining power due to relatively low switching costs and diffused suppliers. In terms of labor, Pandora has again high negotiating power despite significant exposure to Thailand labor market. Company employs 3600 people in Thailand, but most of the positions are within production field, where availability for substitution is high. Moreover, labor is not united under labor unions. It is however sure that bargaining power will grow with the rise of Thailand economy.

Competitive rivalry between Pandora and immediate competitors is distributed unequally. Suppliers and buyers have little power to bargain, while low barriers to enter and threat of substitutes causes high competitive environment.

The primary factor to high degree of rivalry is the number of competitors (appendix 3.22). Even though the number of firms in Pandora markets decreases, the tempo is slow and concentration will not be high for long time. What is more surprising, number of big players is decreasing at even higher pace (except UK). One possible explanation is economic crisis, another – low possibilities to scale the operations.

In terms of local jewelry firms’ revenues, the trend is similar, except again UK (appendix 3.23). Turnover of all US jewelry firms fell at an annual decline rate -3.1% in the last six years and for companies with more than 100 employees CAGR was -3.7%. In Germany figures are similar and only UK experiences some consolidation of larger firms. Negative growth of the market poses another issue – growth could be only at the expense of a rival.

Pandora – financial and strategic evaluation – master thesis – investorship.uk

The dynamics of the production volume confirms parallel with the economic development. US production volume has increased by 22.6% from 1997 to 2000, dropped by -11.6% in 2001, further increased by +4.2% from 2001 to 2005 and decreased by -38.8% from 2005 to 2011. Over fourteen years compound annual decline equals -2.6%, while over last six years decline intensifies to -7.8%. The situation is even worse in Germany, where six years CAGR equals -10.7%.

The collapse in volume is partly offset by an increase in producer prices: six-year annual average of +5.1% in US and +6.4% in Germany. The decrease in local production is substituted by the higher imports, reaching 73% in US, 75% in Germany, 99% in Australia and 49% in UK of total market. Total market size expands across all geographic regions in economic prosperity time, but significantly differs in the period of crisis: UK and US markets plummeted below 2005 level, Germany and Australia experienced an annual growth rate of +0.9% and +8.4% growth respectively.

Industry analysis provides several implications:

· First, industry has neither high fixed costs (rivalry increasing factor) nor high exit barriers (rivalry decreasing). It is therefore healthy to try to expand into new geographical markets, what Pandora in fact has been trying to do;

· Second, jewelry market slows down in developed countries and expands in emerging markets. While Italy market has increased by comparable to old Pandora markets annual growth rate of +0.8%, Japan and Russia grew by CAGR +7.2% and +9.4% respectively and China climbed by impressive +25.5% speed. Naturally, different growth rates and distinct market specifics demand distinctive entrance strategy. Pandora’s experience lies in entering the developed markets, thus entrenchment into emerging markets (definition in appendix 3.25) could take some time and if at all is possible;

Pandora – financial and strategic evaluation – master thesis – investorship.uk

· It is certainly also attractive to enter parallel industries, such as design jewelries, which are growing faster than the fine jewelry market;

· Since the rivalry in the fashion industry is high, one of the best ways to survive is to increase advertising costs and strengthen customer loyalty;

· Vast possibilities to reduce rivalry lay in differentiation. Extensive branding is certainly one of the most direct ways to display company’s authenticity.

1.1.1.3. Critical success factors

Critical success factors are product characteristics valued by the customers the most. Even though company might be competitive within the industry, failure to address the target customer needs could lead to a failure in operations.

In the research of shopping motives Tauber (1972) indicates 14 functional and 12 nonfunctional motives that affect the buying decisions. Sanguanpiyapan and Jasper (2009) recently examined Tauber’s motives at jewelry retail outlet and found out that all motives are statistically important, but jewelry shoppers are more influenced by functional motives. After adjustment (appendix 3.16) six most important motives are assortment, convenience, brand, design, service and price.

The results are inconsistent with other findings. For instance, Jamal and Gode (2001) found out that primary precious jewelry purchase attributes in UK are quality, design, warranty, comfort, price, assortment, brand, value and country of design (COD). Comparing to the previous research, this is a more reliable (due higher sample and smaller standard deviation), but older research (appendix 3.17).

Some explanation to the confusion of why the attributes of luxury goods shopping vary is obtained from Aielo, et al. (2009) survey of 165 students from 8 countries (appendix 3.18):

· The answers differ depending on whether students are asked to evaluate the product or state the motives of purchase decision. Within product evaluation, the ranking of the most important attributes of specialty luxury goods are brand, design, warranty, COD and price, while within purchase decision, the ranking is completely different: design, brand, price, COD and warranty.

· Specialty luxury goods (for example luxury cars, professional photographic equipment and high fashion clothing) are valued very differently from convenience (for example soap, newspapers and milk) and shopping (for example furniture, electronics and inexpensive clothing) goods. While the latter two categories are characterized by price factor dominance, the opposite is true for luxury goods.

· Almost all attributes (except price) within specialty luxury category are more important than in convenience and shopping good categories. It seems that shoppers are ready to spent extra money and pay extra price on luxury goods only when all attributes are at the highest level.

1.1.2. Strategic capabilities

Internal strategic capabilities distinguish Pandora from the competitors permitting company in some respects to meet the necessary minimum requirements to compete in the jewelry market (threshold capabilities) and in some respects, generate superior product (capabilities for competitive advantage). Strategic capabilities are divided into resources (tangible and intangible) and competences to deploy the resources efficiently. These four dimensions merges into four blocks.

Threshold resources:

§ Even though Pandora has an extensive portfolio of different jewelry pieces, only three kinds of jewelry bring more than 5% of total sales: charms, charm bracelets and rings. Therefore, competitive assortment of 1800 designs (with annual introduction of 250 new designs and retirement of 150 old ones) is a threshold and not yet a unique resources;

§ Company built a high network of retail shops (10732 in the end of 2011), which results in stronger competition and consequently higher margins for Pandora. Retailers are widely spread through all continents, meaning inexpensive promotion of Pandora globally;

§ Among financial resources, company has a strong sponsor PE fund Axcel, which potentially could attract money to fund company’s operations. However, they have already taken out a large portion of investment through selling shares in IPO and now focus on investments outside Pandora;

§ Another threshold resource is a diverse range of employees, most of them who are trained in-house;

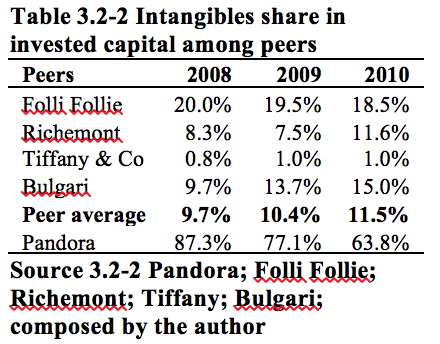

§ From intellectual capital perspective company made several significant acquisitions that added large intangible assets. Intangible value is indirectly measured through goodwill, which equaled 1.9 bDKK, or 24% of assets at 31 December 2011.

Threshold competences:

§ Company has standardized production processes, which are necessary to manage huge resources. Company was acknowledged with ISO 9001: 2008 certification through testing 50 procedures including order processing, purchase and production planning, quality control, customer relations and human resource management.

While threshold activities are important, they do not create competitive advantage. Unique resources underpin competitive advantage that cannot be imitated:

§ First unique resource to mention is a product charm, which brought initial success in 2000 and keeps generating substantial revenues today;

§ Another important physical resource is the four state-of-the-art production facilities, of which two (combined production area of 13000 m2) were opened in 2010. All facilities are located in Gemopolis, a jewelry business zone on the outskirts of Bangkok, Thailand. In 2010 company produced 57 million pieces of jewelry, comparing to 3 million in 2004. In addition, the fifth plant of 10710 m2 area and 70 mDKK investment was expected to be operational in 4Q 2011;

§ Pandora production team in Thailand employs more than 3600 people. Thailand workforce is relatively inexpensive, skilled and trained in-house;

§ Furthermore, in-house designers from Denmark have a long track of success creating various lines of jewelry. Denmark is known for design driven solutions and demanding customers, thus it is a good place to create a design and test the products with the customers;

§ Financially company is empowered to expand and balance the working capital with 2.5 bDKK revolving credit facility, agreed till March 2014;

§ Most precious intellectual resource lay in the brand, which was valued at 1 bDKK, or 13% of total assets in 31 December 2011. In addition, brand awareness among target customers were 51% in 1H 2011.

Core competences:

§ Extensive manufacturing experience (more than 20 years of jewelry manufacturing in Thailand) inevitably leads to the best in class and difficult to imitate practices. Manufacturing processes were controlled and now supervised by the founder;

§ Core competence is also the management’s ability to scale the craftsmanship, produce hand-finished products in mass quantities;

§ Pandora also had superior abilities to successfully enter new markets in a relatively short time period;

§ Despite recent turmoil, still an outstanding financial performance speaks about strong financial consolidation and control functions;

§ Pandora has a difficulty to replicate win-win retail proposition. Pandora offers retailers lower rent expenses by requiring lower selling space (<5 m2 versus an average of 170 m2 in US); high turnover rates per square meter (50 tUSD/m2 versus 6500 USD/m2); high turnover rate (3-4 per year versus 1 per year); gross margins of 55% versus 50%; marketing spend 2.5% versus 4-6%.

1.1.2.1. Value chain

Porter’s (1998) value chain (appendix 3.19) is beneficial twofold: a generic description of activities helps to understand, if there is a cluster of activities providing benefit to customers within particular areas and, second, identification of cost and value of activities helps to detect where managers should focus in order to develop more profitable business model.

Generic description of activities starts with the primary activities that are directly responsible for creation and delivery of a product:

§ Pandora has a warehousing and logistics team, which is responsible for inbound logistics: receiving, storing and distributing inputs. Area’s cost efficiency comes with warehouse facilities being located near production site in Thailand and having internal demand planning department, which collects, consolidates the expectations of the markets and forecast market demand for production capacity;

§ Some of the key Pandora competitive advantages lay within operations, such as 22 years of jewelry manufacturing experience in Thailand, 4 state-of-art plants, founder’s goldsmith skills, cost efficiency in Thailand;

§ The same warehousing and logistics team controls the outbound logistics, which is positive in terms of know-how and data consolidation. However, a decision to distribute the products through central warehouse in Denmark, which serves as a transit location except for US and Australia, seems to be time and transportation cost inefficient. It makes little sense that after central warehouse in Denmark goods travel to 8 local warehouses or third party distributors around the world. This activity can prove to be extremely important both in generating value and in improving differentiation. In many industries control over distribution is proving to be a major source of competitive advantage. As it is shown further down, 50% of the value created in many industry chains occur close to the ultimate buyer. Taken that in consideration, company already made significant step to consolidate external distributors. As a matter of fact, Pandora revenues from third party distribution accounted for 4.9% of total revenues in 2011, down from 54% in 2008;

§ For a long time marketing and sales activities were decentralized, leaving regional partners to make their own decisions. Pandora entered US, Australia and many European markets with the help from local entrepreneurs. Private initiatives were very important drivers for expansion and entrepreneurial character should still form part of company’s DNA. Currently model of marketing and sales is centralized with unified strategies. Company has also changed regional sales directors, who initially started the business. It brings several consequences: (1) abilities to execute unified approach, (2) more control over marketing and sales, (3) coping with scale and higher level of tasks with the help from more experienced management, but on the same time (4) loss of entrepreneurial mechanism and (5) loss of know-how. As indicated before, company sharpens its marketing and sales with superior win-win proposal for retailers`;

§ Pandora delivers a service to end-customers through retailers with franchise contracts. Even though Pandora has all rights and power to demand from the high service standard from retailers, full control is definitely not possible. To ensure that products are displayed in accordance to Pandora retail guidance, and product assortment level reflects the end-consumer needs, company makes 12 sales representative and visual merchandiser visits per year for mono-branded shops, 6 for silver level and 4 for white level shops. Company generally tries to shift away focus from after-sales activities (less than 1% of revenues), keeping it only at the threshold acceptable level (Pandora, 2010a).

Each of these primary activities are linked with support activities, serving as a help to improve the efficiency of primary activities:

§ Pandora’s procurement department ensures that the company has the necessary raw materials by maintaining adequate supplies and keeping in constant communication with production and demand planning teams. Even though the cost of procurement is relatively low, the impact could be significant, as it inspects raw materials and semi-finished goods, establishes relationships with suppliers, checks if the suppliers do business in accordance to the company’s CSR;

§ Technology development (see appendix 3.20 for full analysis) belongs to Pandora’s core competence, since it includes product design, R&D and process development. It is the starting area of Pandora’s vertical integration and primary source for all value chain;

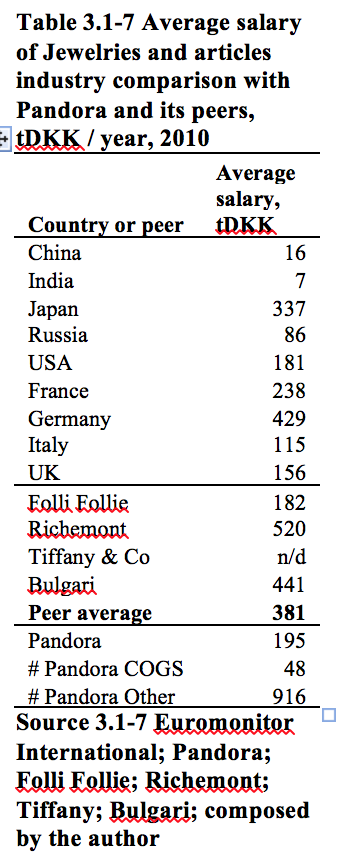

§ Number of employees in Pandora rose from 1288 in 2008 to 5186 in 2011, inevitably making human resource management function of high importance. To address safety and healthy working environment issues, in 2010 Pandora initiated the process of being certified according to OHSAS 18001: Occupational Health and Safety. Average compensation per one employee rose from 108 tDKK in 2008 to 192 tDKK in 2011. Pandora saves on wages in Thailand and attracts experts by paying high salaries to top managers. Whereas typical EU jewelry company spends around 44% of cost of goods sold (COGS) for direct labor cost, Pandora spent only 10% in 2011, up from 5% in 2008. For the nearest future, the savings on labor in Thailand should remain a critical competitive advantage;

§ Historically Pandora infrastructure was decentralized – financial reporting system was based on reporting structures in local markets. Currently Pandora undergoes the process of implementing a more comprehensive group-wide monitoring system. As a result, some of group-wide internal controls are relatively new and might possibly require further adjustments or modifications. From the perspective of finance, company has a widely experienced financial investor Axcel.

Value adding activities are positioned within the supply chain (see appendix 3.21) to identify and separate cost and value activities. Combined picture enables to draw several important conclusions:

· The closer the activity is to the ultimate buyer, the more value is created: retail represents 59% of all value created, wholesale and distribution has a share of 14.1% and manufacturing only 7%;

· Even though Pandora does not participate directly in the retail segment, its prices are half way to complete vertical chains. Typical wholesale jewelry company sells the products for 2.06 symbolic unit, when costs of goods sold equals to one. If the same analogy is applied to Pandora, revenues equal to 3.1 and COGS equal to one in 2011. Full typical mark-up ranged from 4.44 to 5.78;

· Typical EU jewelry attributes 44% of costs of goods sold to material costs, another 44% to direct labor and 12% to other costs.

Breakdown of value added activities shows that Pandora would highly benefit from full vertical integration. There are several moments to consider: (1) current model offers speed and flexibility to launch and change product assortment, (2) capex and management time is focused to production development and capacity increase, but (3) company looses significant portion of value added, (4) has less control over the distribution and brand positioning and (5) significantly depends on variable costs, comparing to scalable fixed retail costs.

1.1.3. SWOT model

After defining business environment and internal strategic capability, overall strategic position could be summarized with SWOT model. In addition, following SWOT analysis should be read as a collection of most important elements in comparison with main competitors:

| Strengths:

§ Experience and state-of-art facilities in manufacturing § Superior design and new product development § Vertically integrated business model with higher profit margins |

Weaknesses:

§ Too high reliance on a sole product – charms § Inability to capture majority of the value added that comes from retailing § Inexperience to implement centralized management model worldwide |

| Opportunities:

§ Growth of affordable branded jewelry segment § Convergence of style and buying patterns in developing markets with developed markets § Higher demand of “create and combine” concept in other product categories |

Threats:

§ Price increases of gold, silver and other main raw materials § Popularity of substitutes, where costume jewelry is of the biggest concern § Further economic downturn in US and Europe |

1.2. Strategic choices

Pandora – financial and strategic evaluation – master thesis – investorship.uk

| 1 ‘No frills’ | Likely to be segment specific |

| 2 Low price | Risk of price war and low margins; need to be cost leader |

| 3 Hybrid | Low cost base and reinvestment in low price and differentiation |

| 4 Differentiation:

a) Without price premium b) With price premium |

Perceived added value by user yielding market share benefits Perceived added value sufficient to bear price premium |

| 5 Focused differentiation | Perceived added value to a particular segment, warranting price premium |

| 6 Increased price / standard value | Higher margins if competitors do not follow; risk of losing market share |

| 7 Increased price / low value | Only feasible in monopoly situations |

| 8 Low value / standard price | Loss of market share |

| Source 2.2‑1 Faulkner and Bowman (1995); Johnson, Scholes and Whittington (2008); composed by the author | |

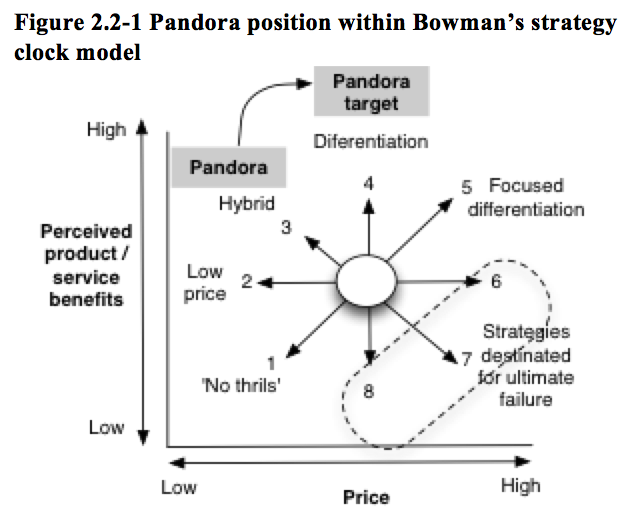

On a business level Pandora needs to decide how to position itself in relation to competitors. Porter (1985) offered three broad strategies to achieve competitive advantage: cost leadership, differentiation and focus. Since the strategies are not clearly defined, another approach, called ‘Bowman’s strategy clock’ by Faulkner and Bowman (1995) is employed.

Strategy clock model (described in 3.2-1) helps to review the bases on which company might achieve competitive advantage. This model extends Porter’s (1985) three strategic positions to eight and explains the options in light of the price and perceived value to the customer combinations. In addition, model helps to identify the likelihood of success for each strategy (Johnson, Scholes and Whittington, 2008).

Pandora is in between “hybrid” and “differentiation” strategies. On one side, company is clearly differentiated with the superior designs, concept “create and combine” and manufacturing quality, on the other side, it tries to fit into affordable price range. Hybrid strategy is advantageous, when (1) much greater volumes can be achieved comparing with those of competitors, so that margins could be still better and (2) as an entry strategy in a market with established competitors.

The hybrid strategy ceased and differentiation started when the Pandora prices started to surpass affordable range. The aim of the differentiation strategy is to offer different benefits at adequate price levels that are comparable with those of competitors. The success applying this strategy is dependent on two key factors: identifying and understanding the strategic customer and identifying key competitors. There are at least two problems that Pandora faced entering this strategy: (1) competitors partly erased company’s distinctiveness by starting to imitate the very successful charms and the concept to “create and combine” and (2) customers were sensitive to further price increase at the time of economic downturn.

In order to sustain the competitive advantage through differentiation, Pandora could go two ways: build the barriers for competitors (particularly imitators) and lock the retail partners by increasing switching costs. What Pandora already does, is (1) taking advantage of imperfect mobility of resources and capabilities, such as intangible brand, image and reputation assets and (2) creating numerous requirements to its retail partners.

Pandora needs to build multiple biases of differentiation to be able to respond to a threat of competitors properly. For instance, focus might be placed not only on design and quality, but also on innovation, which could potentially diversify its product revenue structure and reduce the one product risk. Pandora should also seriously consider establishing several brands to capture low and high price sensitive customers.

In addition, Pandora could use various forms of collaboration. One form is to increase selling power, for example establishing joint research and developing activities. Second form might be to build barriers to entry, for instance joint marketing function and trade association to promote jewelry technical specifications and safety standards. So far Pandora used collaboration to enter new markets with regional sale forces. Company also collaborated with retailers to increase cost efficiency, quality and reliability.

1.2.2. Corporate level directions

On a corporate level Pandora selects products and markets to focus. The Ansoff (1957) product and market growth matrix provides a simplified view of four alternative directions for strategic development.

1.2.2.1. Ansoff matrix

As of today Pandora mostly pursues ‘diversification’ strategy, which resonates in dimensions of markets and products. In terms of product development, Pandora early creates or recreates 150-250 new designs. Recently company also entered non-jewelry category – watches and plans to enter sunglasses. New product development is expensive and high-risk activity due to two reasons: (1) requirement of new strategic capabilities, such as mastering new watch technologies and (2) project management risk, such as postponement to launch distribution of glasses due to quality concerns. To solve these issues, Pandora outsources non-jewelry procurement, assembly and after-sale service.

In terms of market development, Pandora entered 41 new geographic areas in the last three years and expanded to new user markets, such as high-end luxury segment with exclusive LovePods collection.

Diversification strategy is mostly beneficial due to three value-creative reasons:

§ Efficiency gains from economies of scope. Pandora realizes economies of scope by utilizing its intangible resources and competences, such as brand and staff skills in design and manufacturing areas. Synergy is created by using the same selling channels and keeping the same marketing expenses;

§ A raise in market power enables to “squeeze” retailers, attain higher margins and negotiate better prices with suppliers;

§ Spreading the risk, which is especially relevant for Pandora due to high dependency on one product. With incorporation of several other products and markets, Pandora could forego, for instance, economic crisis in developed countries or change of buyer’s style.

In addition to Ansoff model, related diversification must be added to separate vertical (backward and forward) and horizontal diversification. Pandora pursues forward diversification strategy by acquiring distribution activities and further increasing its presence in vertical chain. It is not relevant now, but in future Pandora could also step up in unrelated diversification, development of products beyond current capabilities (Johnson, Scholes and Whittington, 2008).

1.2.2.2. The Boston Consulting Group (BCG) matrix

BCG matrix (Henderson, 1979) is one of the best visual tools to evaluate the balance of the different businesses portfolio. Placement of businesses on two dimensions (market share and growth) also reflects the potential demand for investment and different needs to allocate resources.

Pandora – financial and strategic evaluation – master thesis – investorship.uk

To adapt the model to Pandora circumstances, (1) business units are divided into geographical regions and product categories, and (2) present operational status is separated from the direction, where the businesses are moving.

Since the year 2000 Pandora has at least one clear star – charms and charm bracelets. Only in nine years company reached 15%[4] market share of charms and charm bracelet, valued 9.6 bUSD in 2009. Given the same market size, Pandora market share would swing to 26%[5] in 2010 and remain unchanged in 2011. Pandora’s revenue’s from charms grew four times to reach 4.6 bDKK between period 2008-11 and three times from charm bracelets to reach 0.8 bDKK in the same period. In the structure of revenues, these products occupy respectively 70% and 12% of total Pandora revenues in 2011. The success is attributable to the superior concept and overall charms market growth. Between 2000 and 2009, charms and charm bracelets market experienced CAGR +5.8%, while average growth rate of total fine jewelry market grew CAGR +2.9% in period 1999-2009. The downward sloping arrows in the BCG matrix indicate the changes in the second half of 2011, when Pandora’s charms and charm bracelet revenues declined by -13% yoy.

Among Pandora geographical region stars is US market, which contributed 38% of revenues in 2011 and has expanded 3 times from 2008 to 2010 and +0.8% yoy in 2011. As indicated in the BCG model, US market yields even higher share of the total profits and serves as a base for supporting other product categories and geographic regions.

Question mark cell is problematic due to consumption of high investments. The segment is often highly potential (rapid market growth), but is not very profitable (low market share). One clear questionable Pandora business unit is emerging Asia, another – Americas region without US. While most of the main geographical division revenues shrunk, these constituted growth of respectively 2.2 times and +53% in 2011. Consequently, significant investments are projected within emerging countries. The major jewelry market players already have a solid presence in emerging Asia and collect the profits while developed markets stagnate. Another question mark lays on ring product category, which in terms of revenues expanded 3.8 times in 2010, but decreased by -4.5% in 2011. Watches (the first and single non-jewelry product) are the last questionable segment. It is also the only category without indication of direction, since there are no results of the recent start-up.

Cash cows are business units with high market share and mature market. In Pandora these are UK, Germany, other Europe and Australia. These geographical areas have just shifted from stars and are still not very typical “cash cows”. Revenues from these geographical areas increased by respectively 10.8 times, 3.3 times, 3.2 times and 2.6 times in the period 2008-2010, but then suddenly heavily dropped by -4.4%, -6%, -12.7% and -16.5% in 2011. Such fluctuations are dangerous, inflicting also development of question marks.

Other Pandora jewelry products are on the edge of being dogs or question marks, because for a long time they were not able to generate substantial revenues. In 2011 situation remained unchanged – other jewelry sales increased only by +0.2%. Even though BCG model usually suggests divesting or closing ‘dog’ activities, another way is certainly to restructure the business units and try to extract the potential.

1.2.3. Strategic modes

Any of the strategy directions described in Ansoff matrix might be undertaken in different strategic modes: organic development, acquisition or disposal and alliances. Pandora has expanded with organic development and vertical integration acquisitions. Going forward, organic growth should dominate due to several reasons: (1) company’s strength lies in design and manufacturing, which are relatively easily expandable critical success factors. Company could therefore utilize internal design and manufacturing capabilities; (2) spreading investment over time instead of spending at one time with acquisition; (3) Minimizing disruption to current activities to avoid problems with acquisition integration. Pandora has just consolidated distribution companies and significantly increased manufacturing labor force. It would be reasonable to expect a digestion (Johnson, Scholes and Whittington, 2008).